With the recent rise in inflation and state of competition in the market, a looming question for buyers is what will happen next year to interest rates. For many, the rate they receive will determine the budget for whatever home they choose to offer on.

Interest rates are primarily influenced by the state of inflation and the state of the economy. When inflation runs hot and the economy is strong, we tend to see an upward influence on rates. Even the psychology of investors who believe that inflation will increase in the future can have an upward impact on the rates of today.

However, if COVID-19 variants concerns spike up or other factors that weigh down on economic growth, then we could see rates come back down. Given these unprecedented times, it’s much harder to gauge how the markets will react given that they have been reacting differently during COVID.

Here’s what you need to know:

How has COVID affected interest rates to date?

During COVID, we have seen inflation surge due to all the economic stimulus pumped into the economy by the Federal Reserve, high consumer demand for cars, new housing, home goods, home improvement projects, and all that was required to retrofit their homes into home offices and home schools – and the resulting supply chain issues to meet that demand during a time when manufacturers had to close, consolidate and manage with less staff.

During inflationary times you would expect rates to jump up. However, during COVID, the Fed has been buying Treasury bonds and mortgage-backed securities in enormous volume which has resulted in artificially low rates.

Can you speak to the expectation of an increase in interest rates in 2022?

At the last Fed meeting in September, it was hinted that the Fed could start tapering their bond-buying program as soon as November. The hint of tapering alone caused rates to spike up. The conforming fixed rates moved their lows near 2.500% closer to 3.000%. When the Fed begins to taper, they will decrease their purchases of bonds over a period of time, such as six months.

Without the Fed helping to artificially keep the rates down, rates would likely rise should inflation persist. Should inflation get more out of control, the Fed will likely consider a tightening bias, which includes increasing the Fed funds rate. At the November 3rd Fed meeting, it was officially announced that the Fed would start tapering their bond-buying purchases within the month of November. As expected, rates ticked up on that announcement. It would be expected that rates would continue on that upward path into 2022 should inflation persist.

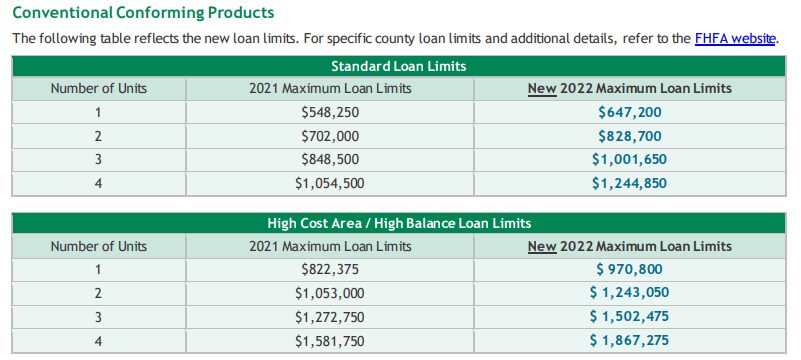

What are the new conforming loan limits moving to in 2022 and when do you expect those to take effect?

The 2022 Fannie Mae conforming loan limits are now in effect. The below chart represents the Fannie Mae limits in the highest cost areas of the United States:

What are the current stumbling blocks you are seeing during the final approval process, specifically after receiving board approval?

A recent stumbling block that we are seeing is if a co-op doesn’t have its 2020 financials completed. Lenders are requiring the 2020 financials in order to close. Some co-ops are still unable to produce them due to COVID-related delays. If they can’t produce the financials, then they can’t close. If they do produce financials at the eleventh hour that are now showing losses outside of bank tolerances, this can be problematic.

How much impact are current appraisals having on deals in New York City?

Low appraisal issues have been coming up from time to time lately. It’s not unusual when coming out of a price dip (as we saw during COVID), that you can see a wider delta between appraised values and current market prices.

The reason is that appraisals are not based upon current market prices. They are based on closed sales that have occurred. The most comparable are those properties that are closest in proximity to the subject property. Appraisers are required to use at least one or two comparables that are located within the same building as their primary comps if they are appraising a co-op or condo. That could be limiting (for example) if the most recent comparable in the building happened during the height of COVID when prices were at their lowest as this can weigh down the value of the appraisal.

This matters as lenders lend based on the lesser of the purchase price or appraised value. If a buyer is doing maximum financing (80-95%) and an appraisal comes in low, they would need to put more money down to stay at their original loan-to-value.

What are the biggest mistakes people make during the mortgage approval process?

Uploading documents into the loan origination system that were not requested can create more complications in underwriting. For example, we ask for the last two months of bank statement and a borrower might upload several months’ worth.

Actions that can have a negative impact on their credit scores such as opening or closing credit cards, applying for next debts, changing up their credit cards greater than 10% of the limit on any one given card. If we have to rerun credit during the process and scores have dropped, that can result in a higher interest rate.

When in the buying process do you suggest potential buyers have their pre-approval done?

You need to be prepared with a pre-approval letter in hand when making an offer. Therefore you should take that step prior to looking at property.

To get pre-approved, connect with a loan officer who will review your financials and help you set a budget for what properties you can afford.

How Platinum Properties can help you:

If you’re a buyer looking to lock in a property before rates jump higher, it’s extremely important to work with an agent who knows the market, knows the city, and has relationships with trusted partners like loan officers and inspectors to make your transaction as smooth as possible.

At Platinum, we are nimble, creative and committed to our clients, we operate without needless layers. Instead, we invest more in our people, our marketing, and our tech, so we are primed to create opportunities.

We know that true innovation comes from the diversity of thought, and we hire to ensure a wide range of experiences, knowledge, and perspectives.

This collaboration strengthens us, both as individuals and as partners, making us smarter and more successful. When our clients succeed, we succeed.